Enviri Corporation Reports Fourth Quarter and Full Year 2024 Results

Enviri Corporation (NYSE: NVRI)

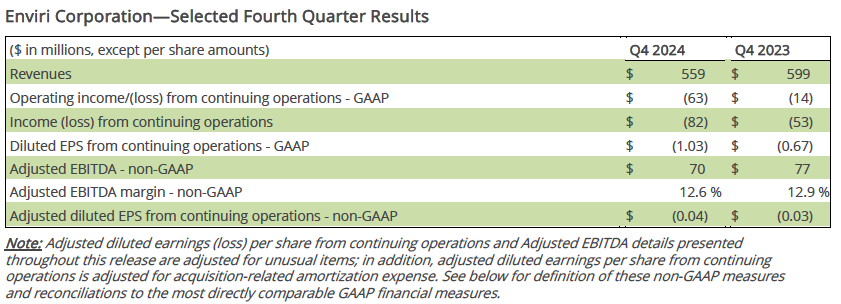

- Fourth quarter revenues totaled $559 million; GAAP consolidated loss from continuing operations of $82 million

- Adjusted EBITDA in Q4 totaled $70 million, an increase of 5% over the prior-year quarter on an organic basis (adjusted for foreign exchange translation and divestiture impacts)

- Net cash provided by operating activities of $36 million and adjusted free cash flow of $8 million in Q4

- Full year 2024 revenues increased 3% on an organic basis

- 2024 GAAP consolidated loss from continuing operations of $119 million; Adjusted EBITDA totaled $319 million, an increase of 11% on an organic basis

- Credit agreement net leverage ratio improved from prior year-end to 4.07x

- Entered into amended credit agreement that strengthens financial flexibility and liquidity

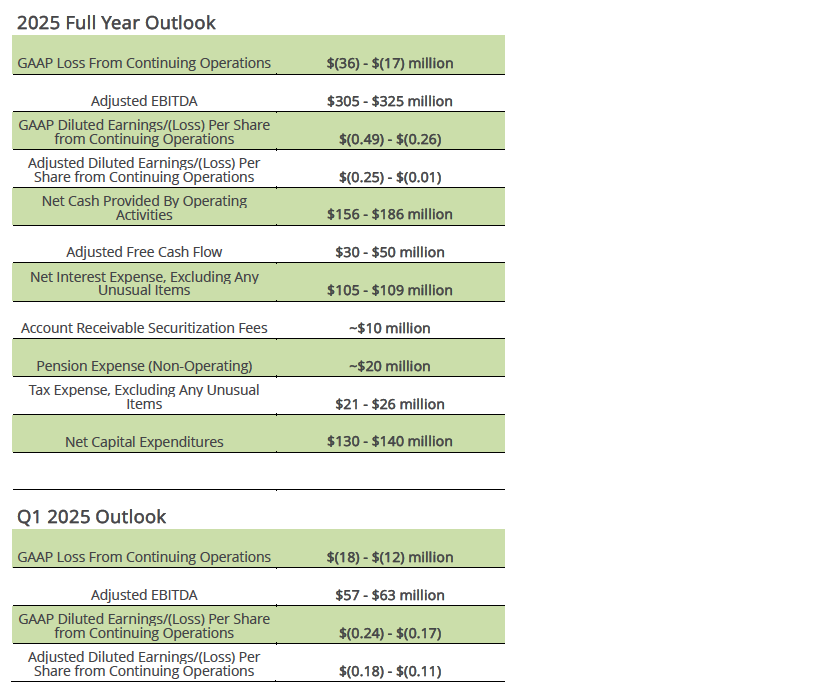

- 2025 Adjusted EBITDA expected to be within range of $305 million and $325 million, higher year-over-year when adjusted for divestitures and FX impact; Free cash flow to increase compared with prior year to between $30 million and $50 million

PHILADELPHIA (Feb. 20, 2025) - Enviri Corporation (NYSE: NVRI) (the "Company") today reported fourth quarter 2024 results. Revenues in the fourth quarter of 2024 totaled $559 million, and on a U.S. GAAP ("GAAP") basis, the consolidated loss from continuing operations for the fourth quarter of 2024 was $82 million. Q4 Adjusted EBITDA was $70 million, a decrease of 9% over the prior-year quarter on a reported basis and an increase of 5% on an organic basis.

On a GAAP basis, the fourth quarter of 2024 diluted loss per share from continuing operations was $1.03, including an asset impairment for an underperforming site and anticipated costs to address an environmental matter in Harsco Environmental as well as additional contract adjustments and a goodwill impairment in Harsco Rail. The adjusted diluted loss per share from continuing operations in the fourth quarter of 2024 was $0.04. These figures compare with a fourth quarter of 2023 GAAP diluted loss per share from continuing operations of $0.67, after strategic expenses and other unusual items, and an adjusted diluted loss per share from continuing operations of $0.03.

“Enviri performed well in 2024, and we continued to focus on consistent execution in the fourth quarter as we faced ongoing headwinds at Harsco Environmental and Rail,” said Enviri Chairman and CEO Nick Grasberger. “The Company realized solid growth in 2024, and our adjusted earnings reached a 10-year high, led by Clean Earth. Strong operational execution, improvement initiatives and a favorable pricing environment drove Clean Earth to once again achieve record profits and margins. Enviri’s other business segments delivered against key objectives during the year, while successfully adapting to various pressures. I’m proud of what the Enviri team accomplished in 2024, and I’d like to thank our employees for their ongoing dedication to our customers and our company.”

“For 2025, our expectations are tempered as weak fundamentals within the global steel market persist and are expected to weigh on Harsco Environmental, while Clean Earth is projected to see continued growth. Importantly, our cash flow is anticipated to improve in 2025, supported by Harsco Rail's execution against certain contracts. We remain optimistic about Enviri’s growth potential and the underlying value within our businesses, and will continue to deliver on our strategic priorities to best position the Company to deliver sustainable value creation for shareholders.”

Consolidated Fourth Quarter Operating Results

Consolidated revenues from continuing operations were $559 million, or 7% below the prior-year quarter due to business divestitures and foreign currency translation, which negatively impacted fourth quarter 2024 revenues by approximately $13 million compared with the same quarter in 2023.

The Company's GAAP consolidated loss from continuing operations was $82 million for the fourth quarter of 2024, compared with a GAAP consolidated loss of $53 million in the same quarter of 2023. Meanwhile, Adjusted EBITDA totaled $70 million in the fourth quarter of 2024 versus $77 million in the fourth quarter of the prior year, a decrease of 9%. Increased Adjusted EBITDA from Clean Earth was offset by lower contributions from the Company's other business segments. FX translation negatively impacted fourth quarter 2024 Adjusted EBITDA by approximately $4 million compared with the prior-year period.

Consolidated Full Year 2024 Operating Results

Consolidated revenues were $2.34 billion in 2024, compared to $2.37 billion in 2023. The change in revenues for the year reflects business divestitures in 2024 and the impact of FX translations. Foreign currency translation negatively impacted 2024 revenues by approximately $29 million compared with the prior year.

The Company's GAAP consolidated loss from continuing operations was $119 million in 2024, while the GAAP consolidated loss in 2023 was $84 million. Adjusted EBITDA reached a 10-year high of $319 million in 2024, an increase versus 2023 ($305 million) despite the negative impacts from divestitures and FX, driven by higher earnings in Clean Earth and Harsco Rail.

On a GAAP basis, the diluted loss per share in 2024 was $1.55, and this figure compares with a diluted loss per share in 2023 of $1.03. These figures include various unusual items in each year. The adjusted diluted loss per share was $0.07 in 2024, compared with adjusted diluted earnings per share of $0.00 in 2023.

Fourth Quarter Business Review

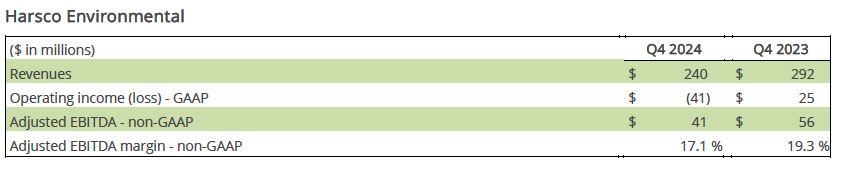

Harsco Environmental revenues totaled $240 million in the fourth quarter of 2024, a decrease of 18% compared with the prior-year quarter. This change is attributable to business divestitures, FX translation, and lower service levels, including the impact of contract exits. Excluding the FX and divestiture impacts, revenues declined 4%. The segment's GAAP operating loss was $41 million and Adjusted EBITDA totaled $41 million in the fourth quarter of 2024. These figures compare with GAAP operating income of $25 million and Adjusted EBITDA of $56 million in the prior-year period. The year-on-year change in adjusted earnings reflects the above-mentioned impacts. As a result, Harsco Environmental's Adjusted EBITDA margin was 17.1% in the fourth quarter of 2024 versus 19.3% in the comparable quarter of 2023.

Clean Earth revenues totaled $241 million in the fourth quarter of 2024, a 2% increase over the prior-year quarter due to higher services pricing. The segment's GAAP operating income was $21 million and Adjusted EBITDA was $36 million in the fourth quarter of 2024. These figures compare with GAAP operating income of $16 million and Adjusted EBITDA of $29 million in the prior-year period. The year-on-year improvement in adjusted earnings is mainly attributable to higher pricing as well as efficiency improvements. As a result, Clean Earth's Adjusted EBITDA margin increased to 15.0% in the fourth quarter of 2024 versus 12.2% in the comparable quarter of 2023.

Harsco Rail revenues totaled $77 million in the fourth quarter of 2024, a 10% increase over the prior-year quarter. This change reflects higher equipment and technology volumes, as well as certain contract loss adjustments in the comparable 2023 quarter, partially offset by lower aftermarket parts volumes. The segment's GAAP operating loss was $32 million and Adjusted EBITDA was $2 million in the fourth quarter of 2024. These figures compare with a GAAP operating loss of $42 million and Adjusted EBITDA of $3 million in the prior-year period. The year-on-year change in adjusted earnings resulted from the above items as well as a less favorable business mix.

Cash Flow

Net cash provided by operating activities was $36 million in the fourth quarter of 2024, compared with net cash provided by operating activities of $68 million in the prior-year period. Adjusted free cash flow was $8 million in the fourth quarter of 2024, compared with $30 million in the prior-year period. The change in adjusted free cash flow compared with the prior-year quarter is attributable to lower cash earnings and working capital changes, partially offset by reduced capital spending.

For the full-year 2024, net cash provided by operating activities totaled $78 million, compared with net cash provided by operating activities of $114 million in 2023. Adjusted free cash flow was $(34) million in 2024, compared with $(12) million in the prior year. The change in full-year free cash flow can be mainly attributed to Harsco Rail, where working capital increased to support certain contracts.

2025 Outlook

The Company anticipates that its 2025 Adjusted EBITDA will be comparable with 2024, while its adjusted free cash flow will significantly improve. Adjusted EBITDA is projected to increase at Clean Earth and Harsco Rail but is expected to decline in Harsco Environmental, mainly as a result of FX translation and business divestitures. Meanwhile, the increase in free cash flow will be primarily driven by an expected improvement in Harsco Rail as certain contract milestones are completed, as well as lower pension contributions.

This outlook contemplates that economic conditions will remain stable and that the Company will benefit from various growth and improvement initiatives. Key business drivers for each segment as well as other 2025 guidance details are below.

Harsco Environmental Adjusted EBITDA is projected to be below prior-year results. Currency impacts, business divestitures, exited contracts and services mix are expected to be partially offset by improvement initiatives, new contracts and product volumes.

Clean Earth Adjusted EBITDA is expected to increase versus 2024 as a result of volume growth, efficiency initiatives and net higher pricing, offsetting the impact of investments and certain items not repeating in 2025 (such as the benefit in 2024 from the reduction in bad debt reserves).

Harsco Rail Adjusted EBITDA is expected to modestly increase versus 2024 as a result of higher demand, pricing and contract adjustments in 2024 not repeating, partially offset by a less favorable business mix.

Corporate spending is anticipated to increase when compared with 2024 mainly as a result of the normalization of incentive compensation as well as non-cash equity compensation.

Credit Agreement and Securitization Facility

The Company recently (February 2025) successfully amended its Credit Agreement to provide additional financial flexibility and liquidity, given the uncertain outlook within the global steel industry. Additionally, the Company amended its Securitization Facility. The changes to the Credit Agreement include revisions to its net leverage ratio, which now ends 2025 at 4.75x and 2026 at 4.25x, before stepping down to 4.00x in the second quarter of 2027. The Securitization Facility was amended to increase capacity from $150 million to $160 million. Further details can be found in the Company's 2024 Annual Report on Form 10-K.

Conference Call

The Company will hold a conference call today at 9:00 a.m. Eastern Time to discuss its results and respond to questions from the investment community. Those who wish to listen to the conference call webcast should visitwww.investors.enviri.com, or by dialing (844) 481-2524 or (412) 317-0553 for international callers. Please ask to join the Enviri Corporation call. Listeners are advised to dial in approximately ten minutes prior to the call. If you are unable to listen to the live call, the webcast will be archived on the Company’s website.

Forward-Looking Statements

The nature of the Company's business, together with the number of countries in which it operates, subject it to changing economic, competitive, regulatory and technological conditions, risks and uncertainties. In accordance with the "safe harbor" provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, the Company provides the following cautionary remarks regarding important factors that, among others, could cause future results to differ materially from the results contemplated by forward-looking statements, including the expectations and assumptions expressed or implied herein. Forward-looking statements contained herein could include, among other things, statements about management's confidence in and strategies for performance; expectations for new and existing products, technologies and opportunities; and expectations regarding growth, sales, cash flows, and earnings. Forward-looking statements can be identified by the use of such terms as "may," "could," "expect," "anticipate," "intend," "believe," "likely," "estimate," "outlook," "plan," "contemplate," "project," "target" or other comparable terms.

Factors that could cause actual results to differ, perhaps materially, from those implied by forward-looking statements include, but are not limited to: (1) the Company's ability to successfully enter into new contracts and complete new acquisitions, divestitures, or strategic ventures in the time-frame contemplated or at all; (2) the Company’s inability to comply with applicable environmental laws and regulations; (3) the Company’s inability to obtain, renew, or maintain compliance with its operating permits or license agreements; (4) various economic, business, and regulatory risks associated with the waste management industry; (5) the seasonal nature of the Company's business; (6) risks caused by customer concentration, the fixed price and long-term customer contracts, especially those related to complex engineered equipment, and the competitive nature of the industries in which the Company operates; (7) the outcome of any disputes with customers, contractors and subcontractors; (8) the financial condition of the Company's customers, including the ability of customers (especially those that may be highly leveraged or have inadequate liquidity) to maintain their credit availability; (9) higher than expected claims under the Company’s insurance policies, or losses that are uninsurable or that exceed existing insurance coverage; (10) market and competitive changes, including pricing pressures, market demand and acceptance for new products, services and technologies; changes in currency exchange rates, interest rates, commodity and fuel costs and capital costs; (11) the Company's ability to negotiate, complete, and integrate strategic transactions and joint ventures with strategic partners; (12) the Company’s ability to effectively retain key management and employees, including due to unanticipated changes to demand for the Company’s services, disruptions associated with labor disputes, and increased operating costs associated with union organizations; (13) the Company's inability or failure to protect its intellectual property rights from infringement in one or more of the many countries in which the Company operates; (14) failure to effectively prevent, detect or recover from breaches in the Company's cybersecurity infrastructure; (15) changes in the worldwide business environment in which the Company operates, including changes in general economic and industry conditions and cyclical slowdowns impacting the steel and aluminum industries; (16) fluctuations in exchange rates between the U.S. dollar and other currencies in which the Company conducts business; (17) unforeseen business disruptions in one or more of the many countries in which the Company operates due to changes in economic conditions, changes in governmental laws and regulations, including environmental, occupational health and safety, tax and import tariff standards and amounts; political instability, civil disobedience, armed hostilities, public health issues or other calamities; (18) liability for and implementation of environmental remediation matters; (19) product liability and warranty claims associated with the Company’s operations; (20) the Company’s ability to comply with financial covenants and obligations to financial counterparties; (21) the Company’s outstanding indebtedness and exposure to derivative financial instruments that may be impacted by, among other factors, changes in interest rates; (22) tax liabilities and changes in tax laws; (23) changes in the performance of equity and bond markets that could affect, among other things, the valuation of the assets in the Company's pension plans and the accounting for pension assets, liabilities and expenses; (24) risk and uncertainty associated with intangible assets; and the other risk factors listed from time to time in the Company's SEC reports. A further discussion of these, along with other potential risk factors, can be found in Part I, Item 1A, “Risk Factors” of the Company’s most recently filed Annual Report on Form 10-K, as updated by subsequent Quarterly Reports on Form 10-Q, which are filed with the Securities and Exchange Commission. The Company cautions that these factors may not be exhaustive and that many of these factors are beyond the Company's ability to control or predict. Accordingly, forward-looking statements should not be relied upon as a prediction of actual results. The Company undertakes no duty to update forward-looking statements except as may be required by law.

Non-GAAP Measures

Measurements of financial performance not calculated in accordance with GAAP should be considered as supplements to, and not substitutes for, performance measurements calculated or derived in accordance with GAAP. Any such measures are not necessarily comparable to other similarly-titled measurements employed by other companies. The most comparable GAAP measures are included within the definitions below and reconciliations of these non-GAAP measures to the most directly comparable GAAP financial measures are included at the end of this press release.

Adjusted diluted earnings per share from continuing operations: Adjusted diluted earnings (loss) per share from continuing operations is a non-GAAP financial measure and consists of diluted earnings (loss) per share from continuing operations adjusted for unusual items and acquisition-related intangible asset amortization expense. It is important to note that such intangible assets contribute to revenue generation and that intangible asset amortization related to past acquisitions will recur in future periods until such intangible assets have been fully amortized. The Company’s management believes Adjusted diluted earnings per share from continuing operations is useful to investors because it provides an overall understanding of the Company’s historical and future prospects. Exclusion of unusual items permits evaluation and comparison of results for the Company’s core business operations, and it is on this basis that management internally assesses the Company’s performance. Exclusion of acquisition-related intangible asset amortization expense, the amount of which can vary by the timing, size and nature of the Company’s acquisitions, facilitates more consistent internal comparisons of operating results over time between the Company’s newly acquired and long-held businesses, and comparisons with both acquisitive and non-acquisitive peer companies.

Adjusted EBITDA: Adjusted EBITDA is a non-GAAP financial measure and consists of income (loss) from continuing operations adjusted to add back income tax expense; equity income of unconsolidated entities, net; net interest expense; defined benefit pension income (expense); facility fees and debt-related income (expense); and depreciation and amortization (excluding amortization of deferred financing costs); and excludes unusual items. Segment Adjusted EBITDA consists of operating income from continuing operations adjusted to exclude unusual items and add back depreciation and amortization (excluding amortization of deferred financing costs). The sum of the Segments’ Adjusted EBITDA and Corporate Adjusted EBITDA equals consolidated Adjusted EBITDA. The Company‘s management believes Adjusted EBITDA is meaningful to investors because management reviews Adjusted EBITDA in assessing and evaluating performance.

Adjusted free cash flow: Adjusted free cash flow is a non-GAAP financial measure and consists of net cash provided (used) by operating activities less capital expenditures and expenditures for intangible assets; and plus capital expenditures for strategic ventures, total proceeds from sales of assets and certain transaction-related / debt-refinancing expenditures. The Company's management believes that Adjusted free cash flow is important to management and useful to investors as a supplemental measure as it indicates the cash flow available for working capital needs, repay debt obligations, invest in future growth through new business development activities, conduct strategic acquisitions or other uses of cash. It is important to note that Adjusted free cash flow does not represent the total residual cash flow available for discretionary expenditures since other non-discretionary expenditures, such as mandatory debt service requirements and settlements of foreign currency forward exchange contracts, are not deducted from this measure. This presentation provides a basis for comparison of ongoing operations and prospects.

Organic growth: Organic growth is a non-GAAP financial measure that calculates the change in Total revenue, excluding the impacts resulting from foreign currency translation, acquisitions, divestitures and certain unusual items. The Company believes this measure provides investors with a supplemental understanding of underlying revenue trends by providing revenue growth on a consistent basis.

# # #

About Enviri

Enviri is transforming the world to green, as a trusted global leader in providing a broad range of environmental services and related innovative solutions. The company serves a diverse customer base by offering critical recycle and reuse solutions for their waste streams, enabling customers to address their most complex environmental challenges and to achieve their sustainability goals. Enviri is based in Philadelphia, Pennsylvania and operates in more than 150 locations in over 30 countries. Additional information can be found at www.enviri.com.